Si proviene da qui

http://www.finanzaonline.com/forum/showthread.php?t=852016&page=50

e da questa istantanea di fine 2007

.

http://www.finanzaonline.com/forum/showthread.php?t=852016&page=50

e da questa istantanea di fine 2007

.

Follow along with the video below to see how to install our site as a web app on your home screen.

Nota: This feature may not be available in some browsers.

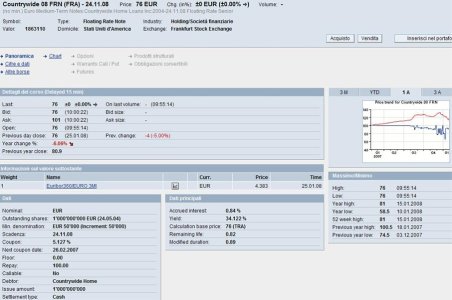

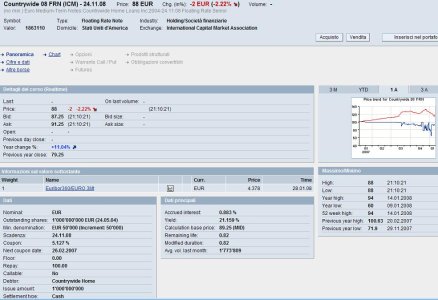

Mark, riguardo i bond di Countryw. ci hai capito qualcosa ?

Tenendo conto di quanto riportava qui http://www.finanzaonline.com/forum/showpost.php?p=15991095&postcount=15 il buon Davide8, Bank of America se ne assume piena responsablità o no ?

Poi: non ho mai acquistato titoli che richiedano un investim. min. di 50.000€, come funziona ? Si acquista 50.000 nominale che (quotando il titolo 78) comporta un esborso di 39.000€ o devo proprio sborsare 50.000 € ?

P.S.

di quei bond si parla qui http://www.finanzaonline.com/forum/showthread.php?t=874605

") ) in quanto le stesse affermazioni di BOA tenderebbero a non accreditare la tesi di una responsabilità de facto, al di là dei meccanismi formali adottati per la fusione, per il debito della società acquisita; le azioni di Countrywide quotano sotto il valore del deal, ad esprimere un certo margine di incertezza circa il fatto che esso venga realmente concluso.

) in quanto le stesse affermazioni di BOA tenderebbero a non accreditare la tesi di una responsabilità de facto, al di là dei meccanismi formali adottati per la fusione, per il debito della società acquisita; le azioni di Countrywide quotano sotto il valore del deal, ad esprimere un certo margine di incertezza circa il fatto che esso venga realmente concluso.Qui la storia bisogna capirla bene, come postava l'ottimo Massimo S. questo titolino qui da uno yield di oltre il 30% !!!!!!!

Sul tema, riprendendo timori che Bank of America possa non rispondere dei bond di Countrywide anche a seguito dell'acquisizione, un interessante articolo del WSJ...

Countrywide Bonds Stir Angst As BofA Avoids Voicing Support

.......................................

When the Countrywide deal was announced, the cost of insuring against a default at Countrywide plunged. Since then, though, the cost has surged to about $425,000 annually for protection on $10 million of Countrywide bonds from $342,000 the day the merger was announced, according to data provider Markit.

The increase is "abnormal," said Matthew Burnell, a bank-credit analyst at Wachovia Capital Markets. He attributes the rise to questions triggered by the Jan. 17 filing. "If there's nothing to it, why don't they say something?" he added.

Countrywide is scheduled to report fourth-quarter results tomorrow, ( QUINDI OGGI) but said last week it isn't holding a conference call with analysts and investors, citing the pending takeover.

Bank of America has said it isn't likely to begin integrating Countrywide's operations until 2009 because the Charlotte, N.C., bank first needs to digest Chicago's LaSalle Bank, which was acquired for $21 billion last year. To skeptics, this is another sign that Bank of America wants to distance itself from any lurking problems.

.......................

Uhmmmm ..............

anche perché altrimenti, se BOA avesse concluso il deal e chiarito la propria intenzione di ripondere per i bond di Countrywide, questi renderebbe assai meno, ti pare ? ma insomma, fallisce o no ?

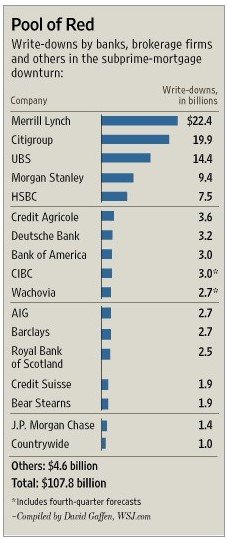

) il 14/02 ci sarà qualche altra perdita ?........UBS, 4° trimestre, -14 miliardi di dollari

(da Bloomberg di oggi)

".....UBS reported about $12 billion of losses directly linked to the subprime market and an additional $2 billion for positions related to the U.S. residential market.........almost double what analysts surveyed by Bloomberg were estimating, and brings the total decline for the year to about 4.4 billion francs, the Zurich-based bank said today in a statement. UBS publishes its official results on Feb. 14."

Aggiornamento su UBS (da qui: http://business.timesonline.co.uk/t...ectors/banking_and_finance/article3279334.ece)

........To make matters worse, UBS revealed that it still owned about $29 billion of bonds and other investments backed by sub-prime mortgages, leaving scope for further writedowns in addition to the $18.4 billion that it has lost so far.