With Jefferies Deal, 'Baby Berkshire' Deviates From Buffett - NYTimes.com

By MICHAEL J. DE LA MERCED

For years, Leucadia National Corporation followed the investment philosophy of Warren E. Buffett, earning the nickname “Baby Berkshire Hathaway.”

But the conglomerate is now deviating from the deal maker’s playbook. It is buying an entire investment bank, which Mr. Buffett has never done.

On Monday, Leucadia agreed to pay $2.8 billion for the remaining shares of Jefferies Group. With the acquisition, Leucadia, which already owns 28.6 percent of Jefferies, will add a growing midsize investment bank to its eclectic holdings. Jefferies is gaining a deep-pocketed partner to help navigate the uncertainty on Wall Street, an environment that has humbled bigger rivals like Goldman Sachs and Morgan Stanley.

“It allows us an even larger foundation to build our company for three, five, seven years with a robust capital base, extremely smart investors as our partners, and do it in a tax-efficient manner,” said Richard B. Handler, the chief executive of Jefferies.

Independent investment banks like Leucadia have been a dwindling breed. Since the financial crisis, new regulations and a sluggish global economy have crimped industry profits. Jefferies’ revenue from fixed-income trading fell 9 percent in the third quarter from the previous three months, mirroring a slump across Wall Street.

With profits slipping, some smaller investment banks are finding it difficult to go it alone. Last week, Stifel Financial agreed to buy KBW in a deal valued at $575 million. The boutique investment bank Gleacher & Company recently put itself up for sale.

“I don’t think anyone would say that this is a robust period for investment banking firms,” Mr. Handler said.

Jefferies has sought to transcend its roots from a firm that traded stocks and bonds. In recent years, the investment bank has worked to raise its profile in areas like mergers advisory, a relatively low-cost business that does not require much capital.

The lack of complexity may be part of the appeal. Leucadia is paying about 1.2 times Jefferies’s tangible book value, a measure of a company’s worth.

Investors are not nearly as sanguine about the firm’s bigger brethren, which have significantly larger balance sheets and face stiffer capital requirements. Goldman’s stock trades at 0.9 times its tangible book value, while Morgan Stanley stands at 0.6 times.

Jefferies does not plan to use its expanded war chest to increase the size of its balance sheet, Mr. Handler said in a conference call with analysts. But it could use its new financial heft to make investments, like the $400 million lifeline Jefferies arranged to bail out Knight Capital, a trading firm.

If the deal is approved, Jefferies will begin a new life as the biggest division of Leucadia, a conglomerate that has little recognition outside Wall Street but has drawn the admiration of value investors.

In the late 1970s, Ian Cumming and Joseph Steinberg took over the company, then a struggling specialized lender named Talcott National. The two men, who were classmates at Harvard Business School, named their new firm after Leucadia, Calif., a seaside town.

Like Mr. Buffett, the partners invested in undervalued stocks, building a diverse group of holdings that includes telecommunications companies, the National Beef Packing Company and the Hard Rock Hotel and Casino in Biloxi, Miss. They even worked with Berkshire, buying a commercial loan company now known as Berkadia Commercial Mortgage.

But the Jefferies deal diverges from the Berkshire model. Mr. Buffett is famously wary of investing in complex financial firms. More than 20 years ago, he was burned by his stake in Salomon Brothers, after a bond trading scandal. When he more recently poured billions of dollars into Goldman and Bank of America, Berkshire received securities that paid out handsome dividends, rather than solely betting the stocks would rise in value.

The Jefferies deal may be more than just a traditional takeover play. The acquisition also provides a potential succession plan. Mr. Cumming will retire, handing over the role of chief executive to Mr. Handler of Jefferies. Leucadia’s president, Mr. Steinberg, will become chairman.

The teams have a long history together. Mr. Handler and Mr. Steinberg have been friends for years, and their firms have done business for more than a decade.

Leucadia first took a stake in Jefferies in 2008, gaining 14 percent of the company and two board seats. The two companies had discussed tightening their bond for several years, and the outlines of a merger took shape several months ago, according to people with direct knowledge of the matter.

Leucadia’s management was particularly impressed with Jefferies’s handling of the recent market scare. After MF Global collapsed last year, investors raised concerns about Jefferies holdings in European government debt. Mr. Handler and his team quickly sold off the bonds and provided regular updates on the firm’s financial health, arresting a potentially fatal stock slide.

“Their ability to manage and grow Jefferies through the elongated financial bubble, successfully navigate the crises that followed where others could not, and protect the firm from the attacks based on false information exactly one year ago with deftness and grace, should comfort all,” Mr. Cumming said in a statement.

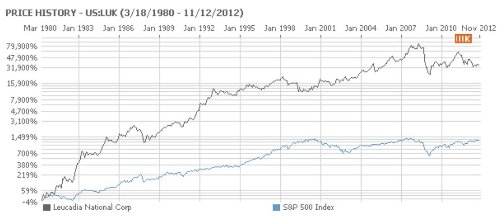

per chi non avesse idea di cosa sia Leucadia, dal grafico del prezzo degli ultimi 30 anni si evince una leggera sovraperformance dei due vecchietti

,

,