giulioron

Nuovo Utente

- Registrato

- 6/5/06

- Messaggi

- 6.910

- Punti reazioni

- 278

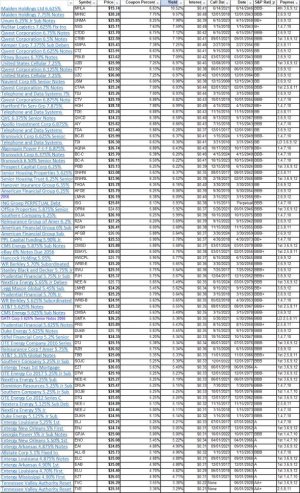

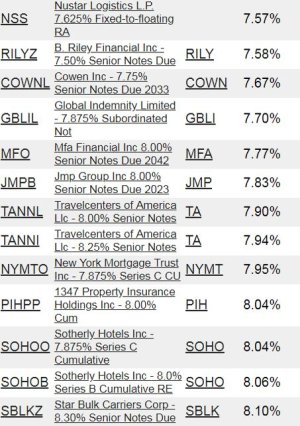

Apro questo thread per differenziarlo da quello relativo alle obbligazioni in USD , che ormai è sovraffollato e per mettere in evidenza strumenti poco conosciuti che comunque possono essere una discreta alternativa di diversificazione , sempre nell'ottica di non esagerare con l'esposizione ( gli all-in non li considero nemmeno)

Qui la definizione di baby bond( spero che tutti capiate l'inglese)

DEFINITION of Baby Bond

A baby bond is a fixed income security issued in small dollar denominations, with a par value of less than $1,000. The small denominations enhance the attraction of baby bonds to average retail investor.

BREAKING DOWN Baby Bond

Baby bonds are issued mainly by municipalities, counties, and states to fund expensive infrastructure projects and capital expenditures. These tax-exempt municipal bonds are generally structured as zero-coupon bonds with a maturity of between eight and 15 years. The muni bonds are usually rated A or better in the bond market.

Baby bonds are also issued by businesses as corporate bonds. Corporate issuers of these debt securities include utility companies, investment banks, telecom companies, and business development companies (BDCs) involved in funding small- and mid-sized businesses. The price of the corporate bonds is determined by the issuer’s financial health, credit rating, and available market data for the company. A company that cannot or does not want to issue a large debt offering can issue baby bonds as a way to generate demand and liquidity for the bonds. Another reason that a company may issue baby bonds is to attract small or retail investors who may not have the funds to purchase the standard $1,000 par value bond.

For example, an entity that wanted to borrow money by issuing $4 million worth of bonds might not garner much interest from institutional investors for such a relatively small issue. In addition, with a $1,000 par value, the issuer will be able to sell only 4,000 bond certificates on the markets. However, if the company issues baby bonds instead for a $400 face value, retail investors will be able to affordably access these securities, and the company will have the capacity to issue 10,000 bonds in the capital markets.

Baby bonds are typically categorized as unsecured debt, meaning the issuer or borrower does not pledge any collateral to guarantee interest payments and principal repayments in the event of default. Therefore, if the issuer defaults on its payment obligations, baby bondholders would get paid only after the claims of secured debt holders were met. However, following the standard structure of debt instruments, baby bonds are senior to a company’s preferred shares and common stock.

One feature of baby bonds is that they are callable. A callable bond is one that can be redeemed early, that is, before maturity, by the issuer. When bonds are called, the interest payments also stop being paid by the issuer. To compensate baby bondholders for the risk of calling a bond prior to its maturity date, these bonds have relatively high coupon rates, ranging from around 5 percent to 8 percent.

Qui la definizione di baby bond( spero che tutti capiate l'inglese)

DEFINITION of Baby Bond

A baby bond is a fixed income security issued in small dollar denominations, with a par value of less than $1,000. The small denominations enhance the attraction of baby bonds to average retail investor.

BREAKING DOWN Baby Bond

Baby bonds are issued mainly by municipalities, counties, and states to fund expensive infrastructure projects and capital expenditures. These tax-exempt municipal bonds are generally structured as zero-coupon bonds with a maturity of between eight and 15 years. The muni bonds are usually rated A or better in the bond market.

Baby bonds are also issued by businesses as corporate bonds. Corporate issuers of these debt securities include utility companies, investment banks, telecom companies, and business development companies (BDCs) involved in funding small- and mid-sized businesses. The price of the corporate bonds is determined by the issuer’s financial health, credit rating, and available market data for the company. A company that cannot or does not want to issue a large debt offering can issue baby bonds as a way to generate demand and liquidity for the bonds. Another reason that a company may issue baby bonds is to attract small or retail investors who may not have the funds to purchase the standard $1,000 par value bond.

For example, an entity that wanted to borrow money by issuing $4 million worth of bonds might not garner much interest from institutional investors for such a relatively small issue. In addition, with a $1,000 par value, the issuer will be able to sell only 4,000 bond certificates on the markets. However, if the company issues baby bonds instead for a $400 face value, retail investors will be able to affordably access these securities, and the company will have the capacity to issue 10,000 bonds in the capital markets.

Baby bonds are typically categorized as unsecured debt, meaning the issuer or borrower does not pledge any collateral to guarantee interest payments and principal repayments in the event of default. Therefore, if the issuer defaults on its payment obligations, baby bondholders would get paid only after the claims of secured debt holders were met. However, following the standard structure of debt instruments, baby bonds are senior to a company’s preferred shares and common stock.

One feature of baby bonds is that they are callable. A callable bond is one that can be redeemed early, that is, before maturity, by the issuer. When bonds are called, the interest payments also stop being paid by the issuer. To compensate baby bondholders for the risk of calling a bond prior to its maturity date, these bonds have relatively high coupon rates, ranging from around 5 percent to 8 percent.