Il 23 di aprile Bloomberg proponeva, allo scopo ultimo di pubblicizzare un paio delle sue funzioni, il seguente - a tutti gli effetti - trading system su credit spread:

La perplessità nasce dal fatto che si tratta di un approccio "sporco": in teoria gli unici casi in cui è possibile fare questo giochino è quando le variabili in ingresso sono cointegrate, cosa che possiamo escludere a priori per

Non di meno vi chiedo: al di là della mancanza di giustificazione teorica, quali sono le vostre opinioni in merito a questo modo di costruire strategie?

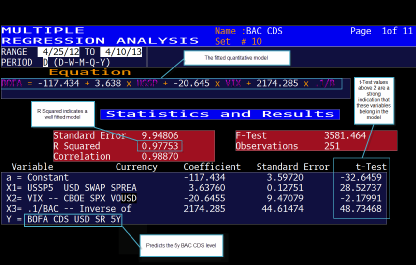

[...] at right is a model for 5-year Bank of America CDS using three simple variables: 1/BAC (the inverse of BAC equity price); the VIX; and 5-year swap spreads. The model [...] has strong explanatory power as the values in the red box on the left show. R-squared is a statistical measure that expresses the predictiveness of a model. It is often called the goodness of fit and ranges in value from 0 to 1. An R-squared here of 0.98 indicates the model is good at predicting Bank of America CDS over time.

The lower graph provides trade entry and exit points for 5-year Bank of America CDS. The residuals are the difference between the actual and predicted levels. A valid model means these differences will gravitate back to zero. For example, if a trader decides to buy Bank of America protection whenever the residual is smaller than minus 20 and sell protection whenever the residual is greater than +20, there would be three trading occasions. Three $10 million trades would have netted about 120 basis points, or $600,000 in profit.

The lower graph provides trade entry and exit points for 5-year Bank of America CDS. The residuals are the difference between the actual and predicted levels. A valid model means these differences will gravitate back to zero. For example, if a trader decides to buy Bank of America protection whenever the residual is smaller than minus 20 and sell protection whenever the residual is greater than +20, there would be three trading occasions. Three $10 million trades would have netted about 120 basis points, or $600,000 in profit.

La perplessità nasce dal fatto che si tratta di un approccio "sporco": in teoria gli unici casi in cui è possibile fare questo giochino è quando le variabili in ingresso sono cointegrate, cosa che possiamo escludere a priori per

- prezzo dell'azione Bank of America Merrill Lynch,

- VIX e

- tasso swap quinquennale

Non di meno vi chiedo: al di là della mancanza di giustificazione teorica, quali sono le vostre opinioni in merito a questo modo di costruire strategie?

")