balcarlo

ama il tuo prossimo

- Registrato

- 24/1/02

- Messaggi

- 22.755

- Punti reazioni

- 3.324

Follow along with the video below to see how to install our site as a web app on your home screen.

Nota: This feature may not be available in some browsers.

Societe Generale rende disponibili su Borsa Italiana (SeDeX) 10 Equity Protection Certificate (con Cap) su azioni e materie prime.

Per continuare a leggere visita questo LINK

Migliora la tua strategia di trading con le preziose intuizioni dei nostri esperti su oro, materie prime, analisi tecnica, criptovalute e molto altro ancora. Iscriviti subito per partecipare gratuitamente allo Swissquote Trading Day.

Per continuare a leggere visita questo LINKOggi i titoli wind tre sono fra i più scambiati ed anche fra quelli con i maggiori rialzi:

cosa ha permesso questa impennata?

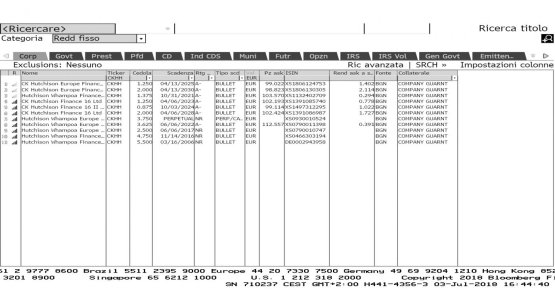

Sono comunque bonds con taglio minimo 100k e quindi adatti sono ad alcuni investitori......

bè.... non capisco questo balzo.... sulla base di questa news...

l'unico che incassa è CHI VENDE.

invece i cinesi di Hutchison avranno fatto debito per questa acquisizione... quindi onestamente adrebbe compreso prima meglio A CARICO DI CHI METTERANNO QUESTO DEBITO.

telecom italia insegna!

ti rendo tutto più facile, CK Hitch. rating A-......quindi i bond Wind, al di là del balzo di oggi, hanno ancora strada da percorrere (verso l'alto) per riallinearsi.....

")

Bella analisi peccato aver capito tutto molto tardi per me...

Vediamo domani se la fanno aprire e dove soprattutto

Saluti

IN che senso se la fanno aprire?

storno corposo

non storna , semplicemente ci sono prese di beneficio dopo il forte rimbalzo di ieri...ovvio che qualcuno passa all'incasso....il tema è : visto che ora Wind Tre è al 100% di Hutchinson , che ha rating A- e paga interessi molto più bassi sui suoi bond, a tendere che succederà ai Cds di Wind? E' ragionevole aspettarsi nelle prossime settimane/mesi un riallineamento dei cds ai livelli della società che ne possiede il 100%? E' verosimile credere che Hutchinson possa migliorarne la struttura finanziaria e magari abbatterne il costo del debito a Suo vantaggio? (ripeto: Hutchinson paga l1,5% sui suoi prestiti, perchè dovrebbe far pagare interessi molto più alti a Wind se è sua al 100%??)